If you are new to the blockchain world and still wondering ‘what is blockchain technology and how does it work’, you have come to the right place. In this beginner’s guide to blockchain, all you need to know has been rounded up in an accessible way: from what is the meaning of blockchain, to its various applications.

What is Blockchain Technology?

When we talk about what is the meaning of blockchain, we’re referring to its core properties as a decentralised and immutable ledger. It securely records transactions and tracks assets across networks. Once the data is recorded, it cannot be altered or deleted, regardless of the number of users with access to it – that’s what gives blockchain its status as a highly secure technology.

Unlike more traditional databases, thanks to how blockchain works, no single individual or authority has control over the system, ensuring transparency and security. Doing away with centralised control, and instead handing the maintenance of blockchain to multiple network participants builds trust in an otherwise fraught digital environment.

How Does Blockchain Work?

Still not completely clear on how blockchain works? Let’s break it down:

Data blocks – every transaction done through this technology is stored in a data block. Think of this as a spreadsheet cell.

Encryption – The data is then encrypted and given a hexadecimal number called a ‘hash’.

Block links – Once encrypted, each block is connected to the ones before and after it, which is where ‘chain’ comes from in the meaning of ‘blockchain’.

Distributed ledgers – The chain of data records how an asset moves between places and people in sequence, and adds this information to a ledger. Copies of the blockchain are distributed between multiple machines (known as ‘nodes’), and all copies must match for a transaction to be considered valid.

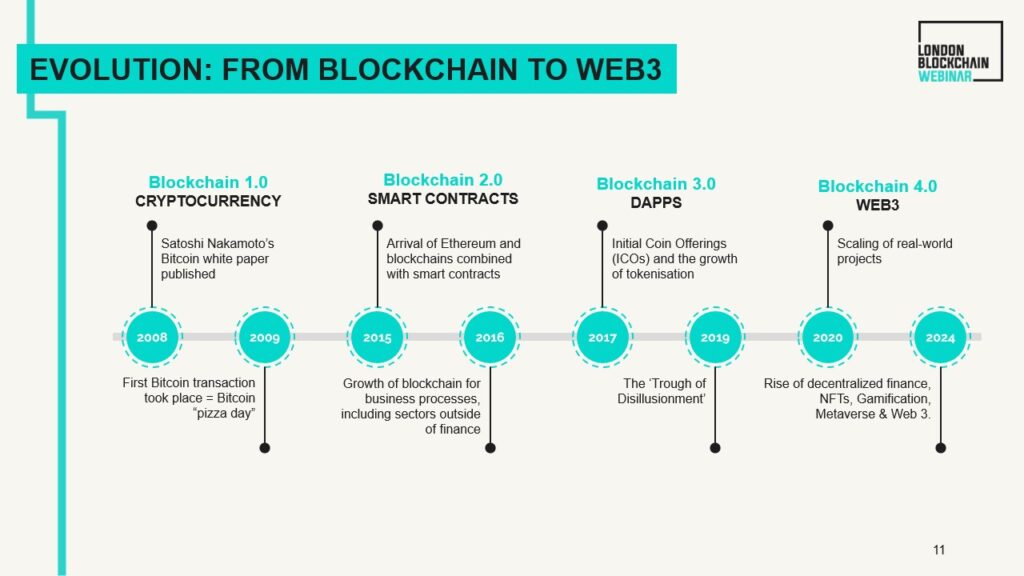

Brief History of Blockchain

Fully understanding the answer to ‘how does blockchain work’ is also tied to grasping the technology’s history.

1991 – Stuart Haber and W. Scott Stornetta introduced early research on cryptographically secured chains of blocks.

2008 – Satoshi Nakamoto released The Bitcoin whitepaper in response to the financial crisis, presenting blockchain as an alternative solution, and the foundation for a peer-to-peer digital currency independent of centralised entities.

2009 – The first Bitcoin transaction was recorded on a blockchain.

2015 – The launch of Ethereum introduced smart contracts, expanding blockchain beyond just digital payments to support other types of decentralised applications.

Present day – Blockchain is a core part of cryptocurrency, Web3 applications, and various global industries.

Are There Different Types of Blockchain?

Another core part of understanding how blockchain works is being able to distinguish between different types. A blockchain network can be private, public, permissioned, or built by a consortium, and the distinction is based on who has access and control to the network.

- Public blockchains like Ethereum and Bitcoin are open to anyone who wants to join and participate. When you think about what is blockchain in crypto, this is the most popular type for crypto assets.

- Private blockchains are controlled by one organisation, which determines who can join, while also carrying out necessary maintenance. This is a popular option for corporations.

- Permissioned or hybrid blockchains are restricted in terms of both participants, and the roles they have. Only certain people can participate, and the type of transactions are controlled. Both private and public blockchains can be permissioned, but it is more common with private networks. Participants will either receive an invitation, or can request access.

- Consortium blockchains are similar to private and permissioned networks, but controlled by multiple organisations. The group of businesses behind a consortium blockchain network share the maintenance and control responsibilities. This type of blockchain is most popular with banking and logistics.

Every one of these network types has its benefits and drawbacks, so understanding how does blockchain work in each context will help you decide what’s best for your scalability, speed, and transparency needs.

What Are The Benefits of Blockchain Technology?

The key advantage of how blockchain works is its ability to provide advanced, end-to-end tracking for a wide range of applications, ensuring that all records remain permanent and verifiable. But that’s just one of the technology’s benefits. Here, we dive deeper into a few:

Trust and security

The data is immutable, access can be controlled, and transactions are approved by multiple computers. Since data is hard to tamper with, users can trust that the information is accurate and unaffected. Not even an administrator can delete a transaction, so there is little to no risk of human error, and the danger of fraud is minimised.

Resilience

The fact that blockchain is distributed means that you are not reliant on storage on one central system. Validation is also made by the network, which negates access issues caused by equipment downtime.

Privacy protection

A private blockchain means only vetted network members can be granted access. However, even on a public blockchain, where users can see the transaction has been made, personal identifying information is kept private to the users involved.

Transparency

Authorised participants can view transactions, which fosters greater accountability. With every entry having a time stamp and being permanently on the record, you can access the full history of a transaction, tracing it back to its origin. This is particularly useful for independently verifying claims in supply chain and government dealings without the involvement of a central authority.

Efficiency

Sometimes a traditional transaction can take days to clear, especially if it has been placed on a Friday, or a holiday. What blockchain technology allows is for smart contracts to run automatically, making processing possible 24/7. This significantly speeds up transactions and avoids office-hour delays. How quickly a blockchain transaction takes can vary, but some take just minutes.

Cost savings

Thanks to how blockchain works, there is no need for third-party verification from a bank, lawyer, or notary. In fact, you don’t need a bank account at all. This not only helps with efficiency but also with costs, as it often means there are no processing fees.

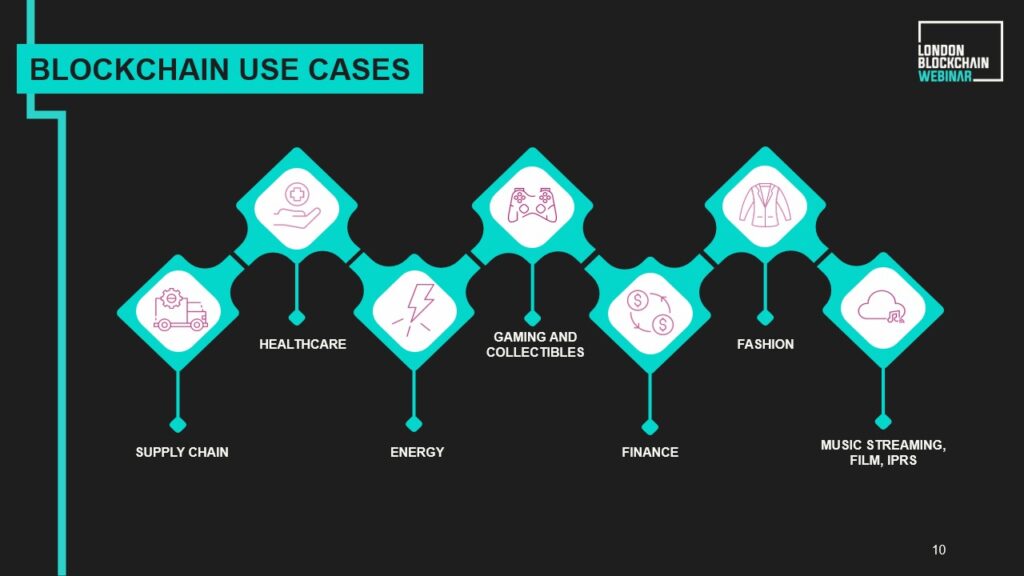

What is Blockchain Technology Used For?

Since the first recorded Bitcoin transaction on a blockchain, the technology has undergone significant advancements, shaping various industries over the past fifteen years.

With its many benefits, blockchain technology is being adopted by more and more businesses and industries every day. In fact, there are now hundreds of thousands of chains.

What blockchain technology is most commonly known for is facilitating the trade and security of cryptocurrencies, like Bitcoin. However, other uses include:

- Education certification – Universities can issue educational certificates using blockchain to prevent fraud and quickly approve verification when individuals apply for jobs or further study. For example, to tackle forgeries, the University of Birmingham has introduced a multi-signature blockchain-based system using Java, JavaScript, and the 2016 credential system from MIT Media Lab.

- Healthcare record keeping – Handling physical records can be extremely inefficient, both in terms of time and cost. Blockchain offers the opportunity to digitalise records, remove the risk of human error, and massively improve efficiencies.

- Supply chain tracking – From food to materials, blockchain can help prove the authenticity of a product and where supplies originated to truthfully use labels such as ‘fair trade’ or ‘organic’. This allows customers to track products on the blockchain from farm to consumption. For example, Nestle Oceania uses Amazon Managed Blockchain to collaborate with partners in their supply chain transparency efforts.

- Fashion – Similarly, when purchasing clothing or accessories, consumers may want to know if what they are buying has been ethically produced, if the product is sustainable, or whether they’re genuine luxury goods. Blockchain can provide this traceability and authentication.

- Music and film streaming – Centralised companies, like Spotify, will pay out royalties to artists once their music is played, but there is often a long wait for these transactions to go through, as there are middlemen (banks) and fees to be deducted. Blockchain could help automate the process using smart contracts to make payments more efficient.

- Voting – In 2018, the US state of West Virginia trialled blockchain to encourage voter turnout and eliminate the possibility of election fraud. Blockchain could help transform voting systems to remove the risk of tampering, reduce the resources required, and speed up the process of securing results.

What is Blockchain Technology in Crypto?

When people first think of what is blockchain technology, cryptocurrency is the first thing that comes to mind. So, exactly what is blockchain in crypto?

In short, blockchain is the foundation of popular digital currencies such as Ethereum and Bitcoin. It keeps track of who owns the coins, while allowing for peer-to-peer payments without the need to go through a bank. It also prevents double spending, and enables the wider spread of decentralised apps (think platforms like Ethereum).

Risks and Challenges of Blockchain: All You Need to Know

Of course, the intricacies behind how blockchain works mean it’s not without its challenges. From high energy consumption and lack of clear government regulation, to requirements for more advanced user knowledge, there are still kinks to be ironed out.

Blockchain technology can also struggle with slower processing speeds compared to more traditional databases. And, while blockchain itself offers great security, exchanges such as crypto payments can still be susceptible to hacking.

Learn more about blockchain interoperability challenges and solutions.

Blockchain and Web3: The Future of the Internet

Unsurprisingly, these two emerging technologies are closely interlinked. How does blockchain work alongside Web3 to shape the future of the internet? It allows for the integration of solutions like decentralised finance (DeFi) and NFTs into the mainstream, helping move away from overreliance on centralised authority.

Discover how Web3 and blockchain technology are building the internet of value.

Learn more about how blockchain works at the London Blockchain Conference

Blockchain technology, a solution originally developed for Bitcoin which has now expanded across industries, is a decentralised, tamper-proof system for recording transactions that continues to grow in popularity.

Of course, there are some challenges still to be resolved with how blockchain works, but its potential for improving security, efficiency, and transparency is bound to have a profound impact on the future.

If you’ve enjoyed this whistle-stop tour through questions such as ‘what is blockchain technology and how does it work’, you can learn more about the ways it’s shaping the future of business from the talks and presentations at the London Blockchain Conference.

Check out our event series and our 2025 conference agenda to learn more. Already convinced? Register for tickets.

Read more: Unlocking the potential of blockchain: Insights from the first London Blockchain Conference Webinar