Key Insights:

- Stablecoins and CBDCs are reshaping digital finance with programmable, regulated systems.

- Rapid stablecoin adoption in payments and cross-border transfers is accelerating global blockchain regulation.

- Stablecoins vs CBDC is a complementary dynamic, not a competition. However, stablecoins will remain crucial for cross-border use cases where CBDCs fall short.

- Banks entering the stablecoin space must choose clear strategies for digital finance leadership.

- CBDCs can deliver secure, interoperable payments if designed with strong privacy and compliance features.

- Africa’s rising stablecoin adoption shows how digital assets can overcome fragmentation and expand inclusion.

- Programmable assets enable proactive, automated blockchain regulation.

- Trust in finance is shifting from institutions to transparent, tech-driven systems.

- The future of money will be shaped by how CBDCs, stablecoins and blockchain regulation evolve together.

The cryptocurrency craze sparked by Bitcoin in the early 2000s gave rise to the digital assets the world knows today. Its epic run even surpassed the global pandemic amid falling investments and a sharp decline in the economy, before eventually plateauing following a series of scandals that raised questions about its real value. Today, Bitcoin’s market cap is merely driven by speculation.

While the hype over Bitcoin has slowly died down, its impact on the future of finance is undeniable. Bitcoin walked, so that assets like stablecoins and central bank digital currencies (CBDCs) could run. Despite lacking actual utility, it became a model for the future of digital money. Now, the spotlight is on these new digital assets, as governments and traditional finance (TradFi) institutions attempt to stay relevant and ensure control in the digital economy.

Stablecoins and CBDCs are promoted to offer stability, reduced risks and real-world utility, but doubts remain over their longevity, considering the path that their crypto pioneer had gone through and other digital currencies that followed suit.

Money Reinvented: The Stablecoin Shift

In recent years, the world has seen stablecoins grow in popularity, prompting central banks and governments to explore ways to incorporate these tokens as a means to diversify their offerings. TradFi’s involvement solidifies that these assets weren’t merely hype, but a serious matter – one that is likely critical in forming the world’s new money.

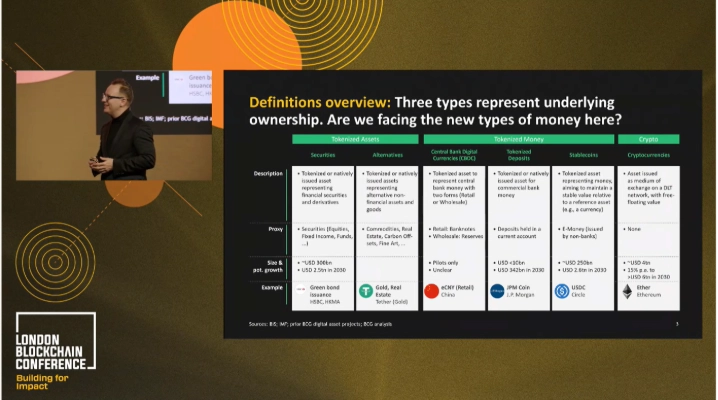

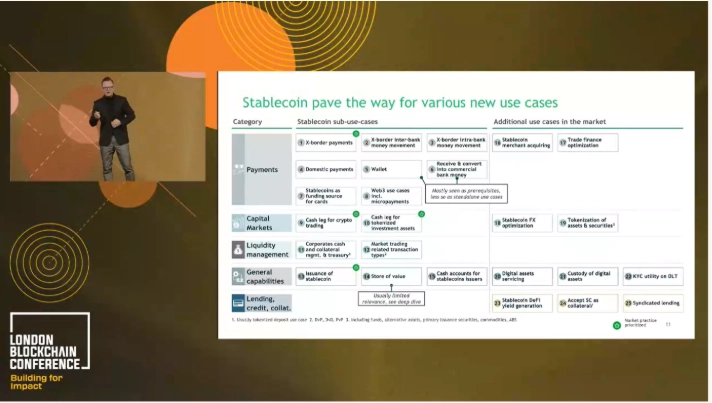

Dr. Bernhard Kronfellner, Partner at Boston Consulting Group (BCG), likened the current state of stablecoins to the early days of the Internet. In a keynote at the London Blockchain Conference 2025, he noted that 92% of stablecoin usage is currently crypto-focused, but that “this will change soon” as bank doubles down on stablecoin implementation in areas such as payments, cross-border transactions, capital markets, lending and liquidity management. Stablecoins are also being explored as a means to counter inflation.

The world’s growing interest in stablecoins had Citi earlier predict that the stablecoin market could attain a $1.9 trillion valuation by 2030.

While banks have the capacity to enter the stablecoin market, doing so would place them in direct competition with the established pioneers of the sector, making their entry challenging, considering that they need to weigh in other factors, including the current state of the economy and consumers’ acceptance of these new tokens.

To address these challenges, Dr. Kronfellner outlined five strategic options to support a smoother market entry for banks:

1. Offer wallets and digital asset custody

2. Be one of the first movers by issuing own stablecoin

3. Create a consortium with others to issue a stablecoin

4. Issue tokenised deposits

5. Hold off on issuing and adopt a wait-and-see approach

Dr. Kronfellner’s recommendations offer a roadmap, but he noted that each bank must chart its own course into the stablecoin market, guided by its strategy, risk appetite and vision for digital finance leadership.

Stablecoins vs CBDCs: Partnership or Rivalry?

While stablecoins have carved out a foothold in crypto and TradFi, CBDCs are emerging as a state-backed counterpart with the potential to reshape payments and monetary policy. Unlike stablecoins, CBDCs carry the full weight of government authority, promising stability and broad accessibility. As both forms of digital currency expand, the key question is whether they will complement each other or compete for influence in the evolving financial landscape.

Dr. Kronfellner said that while the stablecoin market is currently unsettled as government leaders rush to implement regulatory oversight, he anticipates that stablecoins will co-exist with CBDCs in the coming years. Citing the digital euro as an example, he stressed that stablecoins would fill the gaps and address the limitations inherent in CBDCs.

“The digital euro, in particular, is not really allowed to go abroad. So, I would see Europe, in particular, that the digital euro will be used for payments, especially governmental payments, for subsidies,” he said. “For cross-borders, there will be various European-denominated stablecoins…because the cross-border is a better use case.”

The use case for stablecoins within the European Union is not that high, Dr. Kronfellner added, making it easier to co-exist with the region’s CBDC.

At present, hundreds of stablecoins are actively circulating in the market. However, Dr. Kronfellner contends that such a large number is unnecessary, emphasising that only a limited number of stablecoins that consumers can reliably trust are required.

Rethinking Finance Beyond Transactions

While stablecoins are steadily gaining popularity, CBDC is shining under its own spotlight, as more countries are seeing this technology as a tool for faster and safer payment, but its potential reaches far beyond transactions. By combining programmability, transparency and interoperability, CBDCs could reshape how value is exchanged, managed and governed, paving the way for smarter financial systems and more inclusive digital economies.

“Blockchain and CBDCs and stablecoins have the opportunity to create new value and to create new business models,” Minit Money CEO Angus Brown said in a panel discussion at the London Blockchain Conference 2025, where he gave a brief overview of the increasing uptake of usage of stablecoins in Africa.

Brown noted that for CBDCs to thrive, they must overcome the challenges of fragmentation, which is common in regions like Africa, where languages are different and economies have their own set of regulations.

Diego Ballon Ossio, Partner at Clifford Chance, echoed this sentiment, noting the need to understand local frameworks and not merely rely on how fast and massive the current number of transactions using these assets is.

Blueprints for a Smarter Financial System

But realising this potential begins with a thoughtful design. A CBDC’s impact depends not only on its technological foundations but also on how it embeds programmability, privacy, resilience and innovation.

University of Greenwich Professor George Samakovitis said there is a need to have significant types of programmability in value exchange and transaction mechanisms for various use cases, adding that this is crucial in the stablecoins market, and not so much on CBDCs.

In terms of compliance, programmable digital assets open the door to embedded compliance, where regulatory rules are built directly into the asset itself, so that every transaction automatically aligns with regulatory standards, said Samakovitis. Such a concept transforms regulation from a reactive process into a proactive, built-in safeguard that strengthens integrity across the financial system.

“It is doable to hit that sweet spot where you have assets that can be suitably regulated; you can have the role of the regulator in a way being upgraded in a sense that the intervention role is not anymore what we know now to be, and that will allow more latitude to the regulator to do the more important policy work,” he said.

Fnality Services Limited CEO Myles Wright said that programmability creates game-changing opportunities in finance and settlements, including the ability to change how escrow works, improvements in repurchase agreements and in cross-currency exchange.

“The element of innovation is, I think, only a partial piece to the puzzle,” Ballon Ossio interjected. “But effectively, what’s happening is that we’re replacing trust in a third-party…to trust in the technology.”

The New Face of Trust

At the London Blockchain Conference 2025, speakers pointed out that stablecoins and CBDCs are changing the way we think about trust in money and finance. Innovation isn’t just about making payments faster or turning cash into digital form; it’s about rethinking how confidence and control work in the system.

Things that used to rely on banks, clearinghouses, or escrow agents are now managed by code, cryptography, and new governance rules. This is a big shift in how finance works, where trust in technology starts to stand alongside, and sometimes even challenge, trust in TradFi institutions.

In the end, stablecoins and CBDCs are both trying to answer the same question: how can we keep trust in a world that is becoming more digital and decentralised? Stablecoins rely on trust in private companies and the assets they hold, while CBDCs are backed by governments and public oversight. Together, they could shape the future of money, a future where technology, innovation, and regulation work together to make finance more transparent and reliable.

The real challenge isn’t picking one over the other, but figuring out the rules and designs that make this new kind of digital trust safe and accessible for everyone.

Stay ahead in the regulatory curve—explore the full London Blockchain Conference event lineup. Join our next webinar, “From Chaos to Clarity: Understanding the Global Crypto Regulation Wave and Why It Matters for Business” on 10 December 2025, and sign up now to deepen your understanding of blockchain and digital asset regulation.